Tax benefits of oil & gas working interests

One of the most tax-advantaged assets available to U.S. investors.

$100,000 in, $99,000 deducted. Before a single barrel came out of the ground.

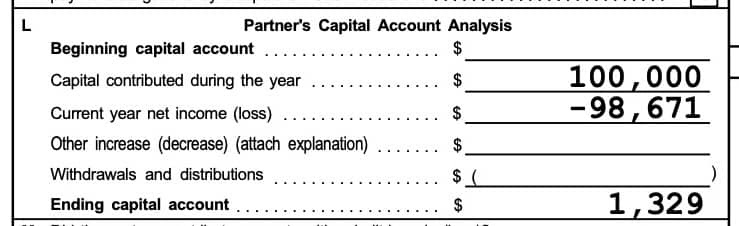

One investor in our most recent drilling fund committed $100,000 and was allocated approximately $99,000 in deductions against their 2025 ordinary income. This is the relevant line from their Schedule K-1:

For an investor in the top federal bracket, that is roughly $37,000 in direct tax savings. Before a single barrel of oil came out of the ground.

Unlike most tax-advantaged real estate, these deductions offset ordinary income: W-2 wages, business income, short-term gains. They do not sit on the sidelines waiting for passive income to absorb them.

The government wants domestic energy developed. The tax code is built to reward the capital that makes it happen.

Benefit 1 Active-Income Treatment

Deductions offset W-2, business income, and short-term gains. Not just passive income.

Active-Income Treatment

Deductions offset W-2, business income, and short-term gains. Not just passive income.

- This is the feature that separates oil and gas from most other tax-advantaged alternatives.

- Under IRC §469, losses from passive activities generally cannot offset wages or business income. That is the rule that blocks most real-estate paper losses from hitting W-2.

- IRC §469(c)(3) carves out a working-interest exception: a working interest in oil or gas is not a passive activity, provided your liability for the obligations of the activity is not limited. Deductions flow straight against ordinary income.

Investors in our funds enter as general partners during the drilling phase, which preserves the working-interest exception and year-one IDC treatment. After completion we convert to limited partners to cap ongoing liability.

Benefit 2 Intangible Drilling Costs (IDCs)

65 to 85% of your investment is typically deductible in year one.

Intangible Drilling Costs (IDCs)

65 to 85% of your investment is typically deductible in year one.

- Under IRC §263(c), operators and their investors can elect to expense (rather than capitalize) the intangible costs of drilling a well.

- In a typical onshore well, IDCs represent 65 to 85% of total cost.

- IDCs include labor, drilling fluids, site preparation, fuel, hauling, and bit repair. Anything that has no salvage value once the well is drilled.

IDCs paid or incurred by year-end for a well that begins drilling by March 31 of the following year are generally deductible in the earlier year (Treas. Reg. §1.612-4). This is what drives the “December close, deduct this year” framing in energy partnerships.

Benefit 3 Tangible Drilling Costs (TDCs)

The remaining 15 to 35% is depreciated, often with bonus depreciation in year one.

Tangible Drilling Costs (TDCs)

The remaining 15 to 35% is depreciated, often with bonus depreciation in year one.

- Tangible equipment (casing, tubing, wellhead, pumping units, tank batteries, flow lines) is capitalized and recovered through depreciation on a seven-year MACRS schedule under IRC §168.

- Bonus depreciation provisions have historically let investors write off a meaningful portion of TDCs in year one, though the bonus percentage has been phasing down under current law.

- Confirm the applicable rate with your CPA. It depends on when equipment is placed in service.

Benefit 4 Depletion Allowance

15 to 30% of gross production revenue, deductible every year the well produces.

Depletion Allowance

15 to 30% of gross production revenue, deductible every year the well produces.

- Oil and gas are exhaustible resources. The tax code recognizes that with a depletion deduction against production revenue. Eligible taxpayers take the higher of two methods each year.

- Percentage depletion (§613A). 15% of gross income from the property for qualifying independent producers and royalty owners. Not limited to basis; it continues after you have fully recovered your original investment.

- Cost depletion (§611 to §613). Allocates your adjusted basis across estimated reserves. Usually the smaller of the two.

Qualifying enhanced-recovery and marginal-production wells can carry a higher effective rate, sometimes into the 25 to 30% range. A number of our units fall in this category.

What about California?

- California does not fully conform to federal IDC rules. CA generally requires IDCs to be amortized over 60 months rather than expensed in year one. That does not eliminate the deduction; it stretches it out.

- Your federal and state K-1s will show different numbers if you live in CA.

- Texas has no personal income tax. New York, Massachusetts, and most other states follow federal treatment. Have your CPA model federal and state returns together.

What about AMT?

- Historically, excess IDCs and percentage depletion were AMT preference items under IRC §57 and could claw back part of the benefit.

- The Tax Cuts and Jobs Act raised AMT exemptions enough that AMT is rarely the controlling factor for individuals post-2018.

- It still needs to be modeled case by case for taxpayers with very large deductions relative to regular taxable income, or with large SALT add-backs.

Is there recapture at the end?

- Technically yes. Prior deductions reduce your basis, and on a sale, that creates ordinary-income recapture under IRC §1254 to the extent of prior deductions in excess of basis.

- In practice, we do not typically sell. Our model is to hold working interests and take distributions from ongoing production for the life of the well.

- No sale, no recapture event. If a deal ever does sell, the rate arbitrage (ordinary-rate deduction today against capital-gain treatment on any spread above basis) is usually still in the investor’s favor.

What should I ask my CPA?

- Almost every question that matters (AMT exposure, state conformity, timing of the deduction, interaction with other passive losses, the right entity) depends on facts only your CPA can see.

- The worst outcome is investing for the tax benefits and then discovering at filing time that your CPA does not understand K-1 reporting from a working-interest partnership.

- We publish a free CPA interview questions guide with a dedicated oil and gas section. We can also connect you with CPAs who regularly handle these K-1s.

Talk through a current deal

If you are evaluating oil and gas as part of a broader tax and cashflow strategy, we are happy to walk through our current offerings and how these mechanics apply in each one.

Bidwell Capital is not a tax advisor, accountant, or law firm, and nothing on this page is tax, legal, or investment advice. Offerings are available only to verified accredited investors under SEC Regulation D. All investments carry risk, including the possible loss of principal. Past performance is not indicative of future results. Tax law changes frequently; rules summarized here reflect federal law as of the date this page was last updated.